Over the past two to three years, global financial institutions have shifted from cautiously monitoring blockchain innovation to actively piloting and deploying Real World Assets (RWA) for banks at scale. In this article, "RWA" means tokenized real-world assets (not "risk-weighted assets" used in banking regulation). This shift is pushing rwa for banks from experiments to production infrastructure for liquidity, faster settlement, and auditable asset transparency.

The momentum is no longer theoretical: major banks are testing tokenized bonds and structured credit, while funds and custodians are integrating on-chain rails into existing workflows. At the same time, a new generation of rwa marketplace operators and enterprise-grade web3 platform providers is building compliant distribution and settlement infrastructure that lets institutions tokenize, custody, and distribute real assets with operational rigor.

This article examines the drivers behind institutional adoption, the integration models banks are using to enter Web3, the compliance frameworks shaping the market, and how ViaHonest enables institutional clients to access and issue tokenized instruments through next-generation infrastructure.

Real World Assets (RWA) for banks: Yield, Liquidity, Transparency, and Operational Efficiency

The rise of tokenized real-world assets is not driven by hype but by measurable financial benefits. For banks and large funds, RWAs provide:

- Enhanced yield opportunities. Tokenized private credit, short-term receivables, and on-chain treasury products create new revenue streams in yield-constrained markets.

- Global liquidity pools. Blockchain rails enable issuers to reach a broader investor base and reduce friction associated with cross-border settlement.

- Programmable transparency. On-chain reporting, audit trails, and cryptographic proofs of asset backing reduce operational risk and improve monitoring.

- Real-time accounting and settlement. Smart contracts eliminate manual reconciliation and accelerate asset servicing workflows.

In this context, rwa for banks is becoming a tool not only for investment but also for improving the mechanics of balance sheet funding, collateral management, and origination pipelines.

Collateral Management and Structured Products

Banks increasingly view tokenization as an upgrade to traditional collateral systems. Tokenized collateral can be monitored in real time, priced more frequently, and rehypothecated with greater auditability. These advantages support:

- Secured lending and repo operations

- Capital-efficient treasury management

- Automated asset-servicing for structured notes and swaps

- Faster onboarding of borrowers and co-lenders

Tokenized corporate bonds, commercial real estate notes, supply-chain receivables, and treasuries are among the early categories gaining institutional traction.

Hedge Funds and Asset Managers Explore New Strategies

Hedge funds, quant funds, and family offices are adopting tokenized assets for different reasons than banks:

- Alternative investment strategies: On-chain private credit, distressed debt, and structured yield notes open new arbitrage and carry opportunities.

- Tokenized securities: Digitized bonds and money-market instruments reduce minimum ticket sizes and enhance liquidity optionality.

- Programmable risk management: Smart-contract-enabled settlement improves exposure monitoring and reduces counterparty risk.

For institutional allocators, rwa for asset managers introduces operational clarity and transparency not found in traditional private markets, making onchain alternatives more attractive.

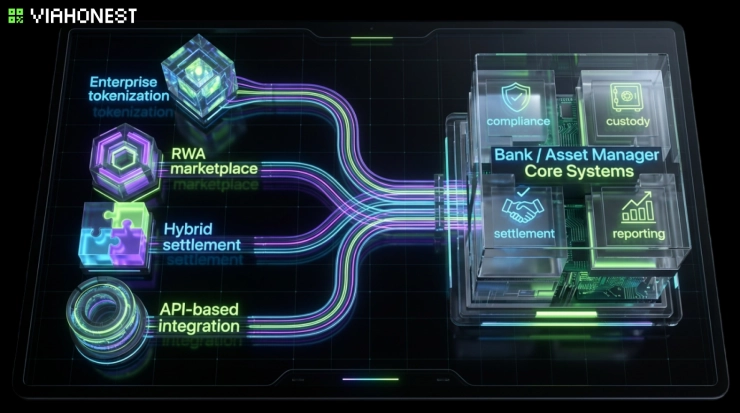

Integration Models: How Traditional Finance Enters Web3

Traditional financial institutions are not embracing Web3 through a single architecture. Instead, they apply multiple integration pathways based on regulation, asset class, internal risk appetite, and legacy system constraints. What follows is a detailed map of the dominant enterprise models that banks, hedge funds, and asset managers use as they move from concept proofs to production-grade tokenization.

Enterprise Tokenization: Bringing Real Assets On-Chain

Enterprise tokenization refers to direct, institution-led issuance of blockchain-based representations of traditional financial instruments. It is the most controlled — and often the most compliant — method of Web3 adoption for large institutions. Banks typically tokenize:

- Fixed-income instruments: Corporate bonds, structured notes, short-term commercial paper

- Sovereign debt: Tokenized treasuries or cash equivalents as funding instruments

- Credit exposures: Secured loans, private credit agreements, revolving facilities

- Real estate: Fractionalized commercial real estate, mortgages, rent-backed receivables.

The institutional motivations include real-time settlement, automated coupon distribution, granular investor KYC, and improved collateral lifecycle management.

Key design considerations:

- Choice of chain: Permissioned chains for regulatory control; public or hybrid for liquidity and interoperability

- Token standardization: ERC-1400, ERC-3643, or bespoke enterprise standards

- Legal wrappers: Tokenized securities are mapped to SPVs, trusts, or direct beneficial ownership models

- Integration with custodians: Ensuring real assets remain legally protected and reflected on-chain

This model is most common among tier-1 banks and government-backed development institutions, which prefer predictable governance and full compliance oversight.

RWA Marketplace models: Institutional Distribution Hubs

Rather than building internal tokenization stacks, many financial institutions leverage external rwa marketplace infrastructure. These platforms operate as compliant, curated distribution channels for tokenized credit, treasuries, and alternative investments.

Core benefits include:

- Pre-tokenized deal flow: Ready-to-underwrite assets without internal tokenization overhead

- Unified compliance architecture: Marketplace-driven KYC/AML, OFAC checks, accreditation screening, secondary-trade controls

- Automated settlement: Smart contracts execute principal flows, coupon payments, and maturity events

- Real-time transparency: Continuous data feeds, audit trails, performance reporting

For banks, marketplaces enable faster entry into Web3, especially for smaller credit desks or asset-liability management (ALM) teams. For hedge funds and asset managers, marketplaces provide diversification and access to alternative yield strategies.

Hybrid Settlement Models: On-Chain Logic, Off-Chain Custody

Most institutional deployments begin with a hybrid architecture that preserves traditional custody while transferring economic and settlement logic on-chain. This approach offers the best of both worlds:

- Underlying securities remain with qualified custodians (e.g., State Street, BNY Mellon, Anchorage)

- Tokenized representations move on blockchain rails

- Regulatory reporting and audits rely on familiar custodial frameworks

- Smart contracts automate settlement and lifecycle events

Hybrid settlement supports:

- Intraday liquidity optimization

- Cross-border repo and collateral mobility

- Automated margining for derivatives and structured notes

- Reduced reconciliation between issuers, custodians, and service providers

In practice, this model significantly reduces operational overhead and can be deployed without restructuring legacy workflows.

API-Based Integration and Infrastructure Partnerships

A rapidly growing trend is for banks and funds to integrate Web3 capabilities through API-first partnerships with specialized platforms. These partnerships allow institutions to "bolt on" tokenization and blockchain rails without replacing internal systems.

Typical components include:

- Tokenization APIs: Automated minting/burning, investor whitelisting, compliance metadata

- Custody APIs: MPC wallets, segregated accounts, hardware security module (HSM) integrations

- Compliance endpoints: Real-time identity checks, transaction monitoring, sanctions screening

- Data + analytics feeds: NAV calculations, price oracles, performance dashboards, risk analytics

- Settlement connectors: Automated reconciliations with the institution's core banking or portfolio management systems

API-based integration lowers the barrier to entry, making it attractive for asset managers, private credit funds, and corporate treasuries.

Permissioned, Public, and Hybrid Blockchain Models

Institutions adopt different chain architectures depending on compliance and desired liquidity:

Permissioned (Private) Blockchains

Used when regulatory control and membership gating are mandatory. Advantages: deterministic access, strict KYC/KYB, confidential data layers. Examples: private credit networks, interbank collateral tokenization.

Public Blockchains

Used when global liquidity and interoperability matter. Advantages: transparent settlement, built-in network effects, composability with DeFi. Popular for: tokenized treasuries, on-chain funds, open-architecture marketplaces.

Hybrid Architectures

Combine private issuance with public-chain settlement or liquidity. Advantages: regulatory safety + market reach. Examples: bank-issued tokenized assets bridged to public networks for secondary trading.

Tokenized Funds and "Wrapper" Models

One of the fastest-growing integration patterns is tokenized fund wrappers. Institutional products include:

- Tokenized money-market funds

- Tokenized private credit funds

- On-chain feeder funds for hedge funds or private equity strategies

- Fractionalized alternatives (real estate portfolios, infrastructure debt, art, royalties)

The token represents a share of the fund and automates:

- Subscription/redemption processes

- Investor qualification checks

- Distribution of dividends and interest

- Proof-of-ownership and audit trails

This model brings historically illiquid assets into a programmable and more liquid digital format.

Regulatory Sandboxes and Pilot Environments

Banks frequently begin their Web3 journey inside regulatory sandboxes provided by:

- U.S. state regulators

- International digital asset regulators

- Central banks and monetary authorities

These controlled environments allow institutions to test:

- Tokenization workflows

- Settlement models

- Investor controls

- Reporting frameworks

- Custody integrations

…without exposing production systems or violating compliance obligations.

Risk and Compliance Requirements in Institutional RWA

Regulatory Alignment: KYC/AML, CFT, SEC, and FINRA Standards

Compliance remains the defining requirement for institutional RWA initiatives. Financial institutions must maintain full adherence to:

- KYC/AML and Countering the Financing of Terrorism (CFT) standards

- SEC and FINRA rules for digital securities

- Custodial licensing requirements for tokenized assets

- Jurisdiction-specific digital asset regulations (state and federal)

Regulators increasingly distinguish between speculative crypto and tokenized traditional financial instruments, but firms must still meet the highest level of reporting and transparency.

Standards for RWA Asset Managers

For large allocators, rwa for asset managers requires:

- Verified asset audits

- Independently validated proof-of-reserves

- Standardized reporting of underlying asset performance

- Full visibility into issuer identity and operational controls

- Periodic third-party assessment of smart-contract and custody workflows

Institutional allocations depend on the credibility and auditability of the asset base.

Risk Categories

Institutions must also evaluate several risk categories:

- Technological risk: Smart contract vulnerabilities, oracle risks, network reliability

- Operational risk: Tokenization workflows failing to match real-world transactions

- Custodial risk: Safeguarding of private keys and multi-signature protocols

- Market risk: Asset price volatility or liquidity mismatches between token and underlying

Mitigation Strategies

Leading institutional platforms implement:

- Independent smart-contract audits

- Segregated institutional custody solutions

- Insurance-backed storage for private keys

- Automated compliance monitoring and reporting

- Transparent disclosure frameworks for issuers

These mechanisms reduce risk to levels comparable with traditional securities infrastructure.

WEB3 platform architecture for institutional RWA: How ViaHonest builds for banks

ViaHonest is developing a next-generation Web3 platform designed specifically to support institutional adoption of tokenized assets. Its architecture focuses on compliance, asset provenance, and secure distribution — the core components required by banks, asset managers, and alternative investment firms.

Tokenization Through NFT-Based Passports

ViaHonest structures each asset with a unique NFT passport that embeds:

- Asset metadata and due diligence

- Legal documentation

- Performance reporting

- Compliance verifications

- Ownership and transfer logs

These passports establish high-integrity provenance, making on-chain assets verifiable and auditable.

Compliance-First Architecture

Regulatory rigor is embedded into ViaHonest from the outset:

- Automated KYC/AML and sanctions screening

- Ongoing transaction monitoring

- Regulator-ready reporting

- Clear frameworks for digital securities classification

This enables institutions to integrate Web3 without compromising legal requirements.

Custodial Models and Secure Infrastructure

ViaHonest supports several institutional custody models:

- Qualified custodians for underlying assets

- On-chain token custody through enterprise-grade wallets

- Multi-party computation (MPC) and key-sharding models

- Segregated ledger views for compliance teams

Institutional-grade security ensures that digital and real assets remain in sync.

API Connectivity and Enterprise Integration

ViaHonest enables banks and funds to seamlessly connect their legacy systems to Web3 rails via:

- Tokenization APIs

- Compliance APIs

- Data and analytics endpoints

- Settlement and reconciliation modules

This allows financial institutions to pilot and scale RWA strategies without rebuilding internal infrastructure.

Access and Distribution

Both sellers (asset originators, banks, and issuers) and buyers (banks, funds, family offices) can join the platform to:

- Tokenize assets

- List institutional-grade offerings

- Purchase tokenized instruments

- Participate in primary and secondary distribution

Institutions interested in early access or custom B2B pilots can connect directly with ViaHonest to explore tailored onboarding paths.

The Convergence of TradFi and DeFi Through RWA

Tokenization is becoming the connective tissue between traditional finance and decentralized infrastructure. Institutions are entering Web3 not out of curiosity, but because tokenized real-world assets offer meaningful improvements in liquidity, settlement speed, transparency, and operational efficiency. As banks, hedge funds, and asset managers expand their engagement, institutional RWA stands out as the primary bridge linking legacy systems with programmable financial rails.

Platforms like ViaHonest are accelerating this convergence by delivering secure infrastructure that meets the compliance and operational requirements of the world's largest financial organizations. The result is a profound shift in how assets are issued, traded, and managed — a shift that is laying the foundation for the next generation of global finance.

Institutions ready to explore tokenization, access institutional-grade RWA opportunities, or launch pilot integrations can connect with ViaHonest and start building the future of enterprise tokenization today.